Macroeconomic Analysis

Global macroeconomic trends and regime shifts stand at the centre of everything we do.

We publish only when we have a view, or to announce changes in our Reference Portfolios. If our analysis is wrong our performance will reflect this. And then we fix it – at least we try.

Currency Markets

There is only one exchange rate connecting any two complex economies. The range of possible transactions settled through this one price is enormous, ranging from travel money to trillions in cros-border investments. We like the challenge.

Systematic Strategies and Portfolios

Most systematic factor strategies in our database have been running out-of-sample since at least 2016. Combining them into strongly performing, uncorrelated and risk budget controlled Portfolios remains the main objective. Identifying the best factor stretegies for the prevailing regime remains the main challenge.

No Blackbox

The platform offers granular details of all our Systematic Macro Portfolios (SYMAP) – right down to the level of code snippets for individual factor strategies. Every portfolio and factor strategy is updated overnight, with daily execution tables. A number of interactive tools help with strategy ranking and selection.

Bespoke Projects

We develop bespoke strategies and portfolios for “ALPHA” subscribers. Bespoke strategies can only be accessed by their owners. Access rights are enforced at API level as well. Subject to available capacity, we help our clients with custom research projects.

The Challenge

Among many, here is one example of what keeps us busy:

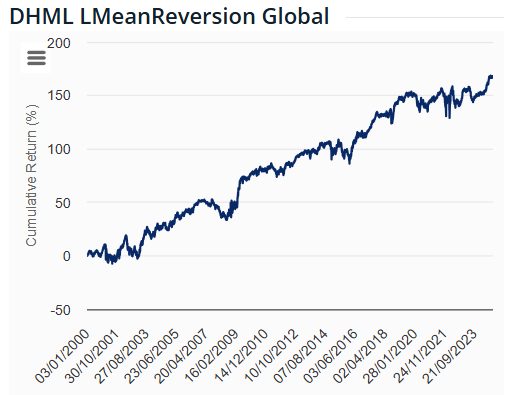

The factor strategy shown in the chart, (number 12 out of a current total of more than 4000) has been running live since late 2014. The 10-year out-of-sample performance is just as good as the in-sample returns from 2000-2014. The theoretical underpinning of long-term mean-reversion is strong as well, as there is little statistical doubt that currencies oscillate in the long run.  But the drawdowns have been brutal. And it took about 5 years for the strategy to clearly break above the most recent 2019 highs.

But the drawdowns have been brutal. And it took about 5 years for the strategy to clearly break above the most recent 2019 highs.

How can an investors harvest this macroeconomic alpha without getting wiped out by these drawdowns and periods of poor performance?

Constructing diversified portfolios of strategies certainly helps, but raises more questions. Equal allocation or not? Dynamic risk budget weights, but how? Which macroeconomic variables can help to produce high-quality performance forecast for mean-variance optimisation? What exactly is the macro regime in which this strategy fails?

Many more questions than answers. And a constant threat of overfitting.

We love the challenge.